Have You Ever?

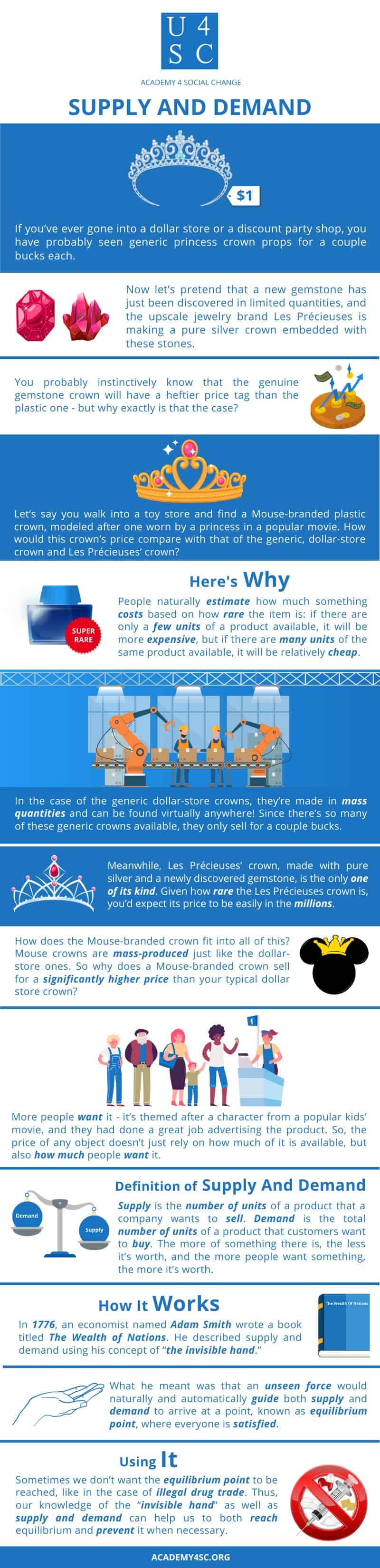

Have you ever wondered about how companies decide on prices for their products? Well, if you’ve ever gone into a dollar store or a discount party shop, you have probably seen generic princess crown props for a couple bucks each. Now let’s pretend that a new gemstone has just been discovered in limited quantities, and the upscale jewelry brand Les Précieuses is making a pure silver crown embedded with these stones - it’s currently the only one of its kind in the world. You probably instinctively know that the genuine gemstone crown will have a heftier price tag than the plastic one - but why exactly is that the case?

Keep that question in the back of your mind for now while we explore another scenario. Let’s say you walk into the toy section of a store and find a Mouse-branded plastic crown that’s themed after the latest Ice Queen’s tiara. How would this crown’s price compare with that of the generic, dollar-store crown and Les Précieuses’ crown?

Here’s Why

People naturally estimate how much something costs based on how rare the item is: if there are only a few units of a product available, it will be more expensive, but if there are many units of the same product available, it will be relatively cheap. In the case of the generic dollar-store crowns, they’re made in mass quantities and can be found virtually anywhere! After all, they’re mostly made of plastic, a plentiful material here on Earth. Since there’s so many of these generic crowns available, they only sell for a couple bucks. Meanwhile, Les Précieuses’ crown, made with pure silver and a newly discovered gemstone, is the only one of its kind. Given how rare the Les Précieuses crown is, you’d expect its price to be easily in the millions.

Now how does the Mouse-branded crown fit into all of this? Mouse crowns are mass-produced just like the dollar-store ones, and they’re also mostly made of plastic. So why does a Mouse-branded crown sell for a significantly higher price than your typical dollar store crown? Well, more people want it - it’s themed after a character from a super-popular kids’ movie, and the Mouse has probably done a great job advertising the product. So, the price of any given object doesn’t just rely on how much of it is available, but also how much people want it.

Supply and Demand

Supply is the number of units of a certain product that a company wants to sell. Demand is the total number of units of a certain product that customers want to buy. Here’s a very simplified understanding of supply and demand: the more of something there is, the less it’s worth, and the more people want something, the more it’s worth.

How It Works

Adam Smith was one of the first economists to explain supply and demand in depth.

In his 1776 book titled The Wealth of Nations, Smith described supply and demand using his concept of “the invisible hand.” What Smith meant was that an unseen force (an “invisible hand”) would naturally and automatically guide both supply and demand to arrive at a point where everyone - both buyers and sellers - is satisfied. That point where everyone is satisfied is known as the equilibrium point, the price at which the amount of product that companies want to sell perfectly equals the amount of product that customers want to buy.

During Smith’s time, there was a great debate between famous economists over how trade should be regulated in order to best serve the people. Smith was a supporter of the laissez-faire approach. In French, laissez-faire directly translates to “let do,” meaning that the government should not interfere with trade using laws or restrictions, and should instead simply let the natural force of the “invisible hand” run the market. By leaving the market to its own devices, Smith believed that the market would function more efficiently.

Using It

The influence of supply and demand is not limited to the world of economics - supply and demand can also impact legislation and other actions of the government. For example, take a look at the various approaches to tackling the problem of illegal drug trade. Using only the supply-targeted approach, the government would aim to implement stricter regulation of all drugs, heavier punishment for the possession and selling of illegal drugs, and increased police personnel dedicated to busting drug trade. Essentially, the supply-targeted approach tries to limit the amount of illegal drugs available on the market. Using only the demand-targeted approach, the government might spend more resources on psychological research to identify people who are predisposed to drug addiction before addiction actually happens, increase the quality of rehabilitation centers, and improve anti-drug education in schools. Essentially, the demand-targeted approach tries to either prevent people from being addicted to drugs in the first place or treat their existing addiction.

As you can see, although Adam Smith’s “invisible hand” principle theorizes that a market left alone will eventually reach an equilibrium point where the amount of product available for sale perfectly equals the amount of product that customers want to buy, sometimes we don’t want that equilibrium to be reached, like our case of the illegal drug trade. Thus, our knowledge of the “invisible hand” as well as supply and demand can help us to both reach equilibrium when we want it, and prevent equilibrium when necessary.